THE MOODY’S RATING CUT

PLUS: INTRIGUED WITH IZEA

MOODY’S CUTS U.S. CREDIT RATING

Moody’s Ratings cut the United States’ sovereign credit rating one notch to Aa1 from Aaa, citing the growing burden (including the GOP revolt burden) of financing the federal government’s budget deficit and the rising cost of rolling over existing debt amid high interest rates.

You can also watch the video below:

Note that the Moody’s announcement caused a spike in interest rates which has continued in early Sunday T-Bond trading:

…and to boot re interest rates…

An Emerging GOP Revolt Makes Cutting spending Tougher:

There is much press regarding the difficulty House Speaker Johnson is having at getting a budget bill passed. Congressman Chip Roy presented concerns about the spending and then was interviewed by Steve Bannon:

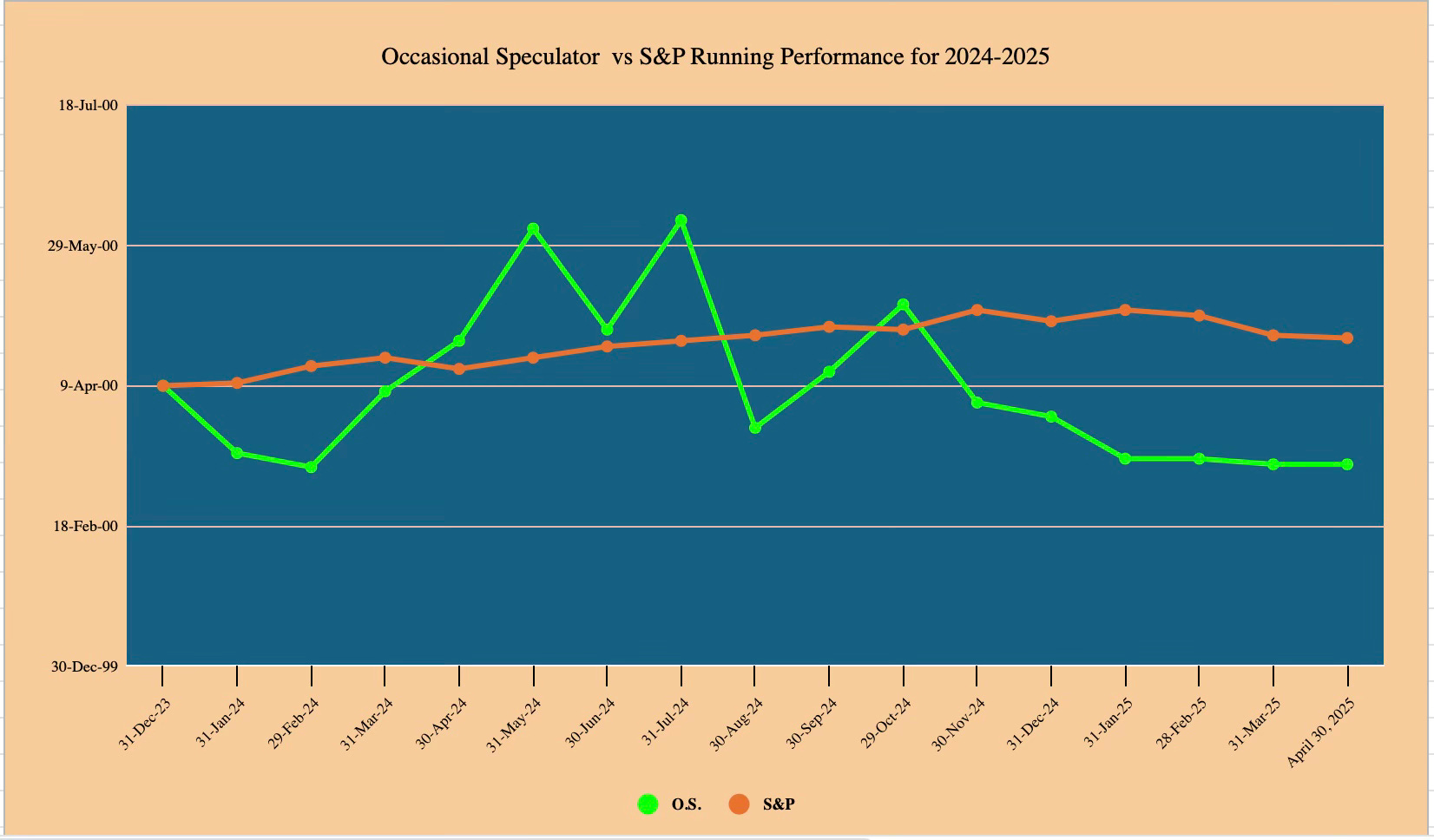

We conclude that the recent up surge in interest rates is likely to continue as long as the projected deficits are as large as Chip Roy demonstrates that they are.

THUS

We continue to recommend therefore shorting the 30 Year Jun T-Bond @ 112 22/32 and also buying the March 2026 95.3125 SOFR puts selling at $100…

…and we continue to recommend shorting the Japanese 10 year future- the Jun JGB @ 139.36 (as of May 18th)

BUY IZEA @ $2.75- with a Thank you to Grant’s

I have subscribed to Grant’s Interest Rate Observer for many years. While the site gives an excellent review of the financial markets in general, I like it primarily because every once in a while, they dig down and research a smaller, out of favor stock that exactly fits my long term speculative strategy. For example it was Grant’s that introduced me several years ago to Hallador (HNRG@ $19.23 which we continue to recommend as a BUY) which I bought @ 60 cents (I ended up having to sell the stock to generate venture capitalistic cash @ $1.80- but that’s another story)…

But Saturday 5/17 while at the poker table (winning session) I picked up the May 9, 2025 issue of Grant’s and whaddya know- Grant’s comes through again recommending the ‘influencer advertising concern IZEA’…

We agree with Grant’s.

Therefore…

BUY IZEA Worldwide, Inc. (IZEA) @$2.75.

As the Yahoo Finance IZEA page indicates IZEA, ”together with its subsidiaries, provides software and professional services to connect brands and content creators…( in the US)…. The company offers IZEA Flex, its flagship platform for managing enterprise influencer marketing….”

Here is why we like it:

The company in September 2024 hired a new CEO Patrick Venetucci (who knew the company already from being on the board)

Venetucci has brought the company to the brink of profitability- a pretax loss of $8.8M in Q3 to a pretax loss of $4.8M loss in Q4 to a pretax loss in Q1 of ONLY $142K!

The market cap of $46M compares with 12/31/2024 book value of $48M and CASH of- wait for it- $51M!

The company is in a growth industry- internet influencer marketing- the CEO pulled out of all markets except the US market

The company- 18 years old- has established brands….to quote the Q1 Earnings call…” We won business from Nestle, Acer, Jeep and more. Our sales pipeline is trending up with larger opportunities from higher-quality clients.

We produced exciting new work for Clorox, Carnation Breakfast Essentials, Matin Kim, Academy Sports, and Coursera to name a few.”IZEA is buying back a chunk of its own stock for the next month. This would reduce the number of shares by 15% if enough sellers take the deal

Here is the Link: IZEA Earnings Call

We should note that we cannot find any analysts estimate for 2025 earnings but the 6 reasons above why we are positive are enough for us to recommend.

ENDEAVOUR SILVER UPCOMING REVENUE GROWTH- WOW!

Endeavor Silver starting May 1 , is officially ramping up production at its huge new Terronera silver mine. The company expects Terronera to reach full production by August of 2025. This translates into Q4 revenues of 5M silver equivalent ounces. Assuming (conservatively) no change in the current $32+ per ounce price this will translate into the following quarterly revenue projections as follows:

Q4 of 2024 reported- $42M

Q1 of 2025 just reported- $63M

Q2 of 2025 (our estimate)- $80-90M

Q3 of 2025 (our estimate)- $110-130M

Q4 of 2020 FULL PRODUCTION- $160-170M

Note that with each quarter, profit margins should increase. Furthermore, the average revenue projections for 2026 of the 5 analysts covering EXK is not a mere $640M, but rather $757M and the average earnings per share estimate for 2026 is 35 cents. This explains why those same analysts expect EXK’s price currently @ low $3.25 (missed Q1 earnings estimates reporting a loss) to hit a target of $6.08- a gain of 87%- within a year. And what if the silver price is many analysts expect comfortably exceeds today’s $32..25?

EXK remains a STRONG BUY @$3.25.

WHAT I LEARNED

TRUMP’S MIDDLE EAST PEACE PROGRESS:

LINK to Middle East Article HERE

ANDY MAGUIRE EXPLAINS THE LAST SUCCESS BY CHINA OF BUYING UNDERPRICED GOLD- THIS IS OVER IN JULY 1 (i.e. SIX WEEKS). Also China is opening vaults in other countries to buy, sell, and price gold OUTSIDE of western influence

ALASDAIR MACLEOD’S TWO LATEST,